Handling of Goodwill

Estimate of Goodwill

Goodwill ⇒ Posted as merger compensation (Note 1) to the corporations to be acquired exceeds net asset value (Note 2) of corporations to be acquired

For the data : Is of treatment of goodwill from the merger, Please refer here.

| Note 1: | Merger compensation is the amount obtained by multiplying unit price of one investment unit of the new investment corporation, which is the compensation for the merger, by the number of investment units allocated. |

|---|---|

| Note 2: | In accordance with the Accounting Standards for Business Combinations, assets and/or liabilities of corporations to be acquired will be assumed based on their market value. |

Accounting Treatment of Goodwill

Goodwill is recorded as intangible assets on the balance sheets.

| * | For accounting purposes, it will be regularly amortized through the fixed amount method for twenty years. The amortization costs will be recorded as operating expenses in the statement of income and retained earnings. |

|---|

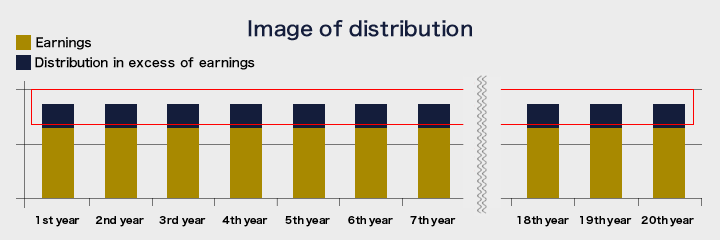

Effect of Goodwill

The goodwill amortization is considered as expenses for accounting purposes. However, since it does not accompany cash outflows, distribution in excess of earnings is conducted so as not to affect the level of distribution.